Risk-On Sentiment Regains Control as Data Downplays Severity of Tariff Shock

World threat sentiment continued to enhance final week, with main fairness indices staging sturdy rallies as investor nervousness over the fallout from tariffs eased. The strong US non-farm payroll knowledge was a key turning level, reassuring markets that the early financial influence of the commerce shock was not as damaging as initially feared. Added to that, there have been indicators of progress on a number of commerce negotiation fronts, together with a possible thaw in US-China relations.

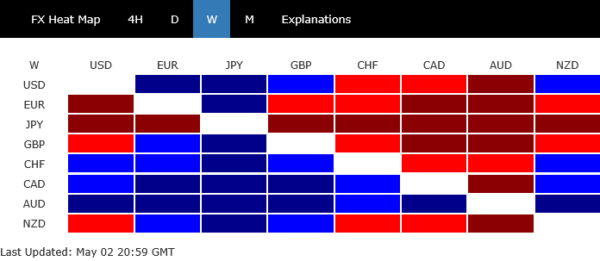

Within the foreign money markets, Aussie was the highest performer, buoyed not solely by enhancing threat urge for food but in addition by stronger-than-expected inflation knowledge, which suggests the RBA’s easing path could stay gradual. Loonie adopted as second benefiting from political stability after the Canadian elections. Swiss Franc ranked third.

However, Yen fell essentially the most, beneath stress from a dovish BoJ that downgraded its development outlook. Euro was the second weakest performer, reversing a few of its earlier energy regardless of a sharper-than-expected acceleration in core inflation. Sterling additionally lagged as third worst. Greenback and New Zealand Greenback ended the week in the course of the pack.

US Shares Erase April Losses as Payrolls Soothe Development Fears, Fed Lower Odds Fall

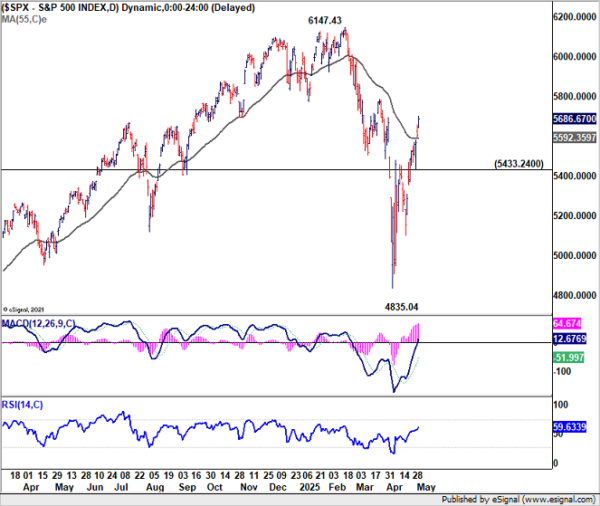

The US markets have decisively moved previous the turmoil sparked by the reciprocal tariff bulletins in April. Investor confidence has absolutely recovered, particularly in equities with each S&P 500 and NASDAQ reversed all losses from April. S&P 500 even notched a exceptional 9 consecutive days of beneficial properties, its longest successful streak since 2004. DOW can also be on monitor to finish a full reversal.

Sentiment had wavered briefly after Q1 GDP confirmed an surprising contraction. Nonetheless, these considerations have been largely alleviated by April’s non-farm payroll report, which confirmed strong job creation and secure unemployment. The info means that whereas commerce disruptions stay a priority, the labor market is resilient and the broader economic system continues to be on sturdy footing. This has helped markets conclude that the fast financial harm from the tariff standoff is extra modest than feared.

Wanting forward, the 90-day tariff truce, set to run out in early July, turns into the subsequent main milestone for buyers. There are tentative indicators of progress on commerce negotiations, together with recent indicators from China that it might be open to returning to the desk. Whereas expectations for a zero-tariff consequence stay low, the worry of escalation to a worst-case state of affairs has clearly eased. Markets look like pricing in a extra constructive path, even when slow-moving and politically complicated.

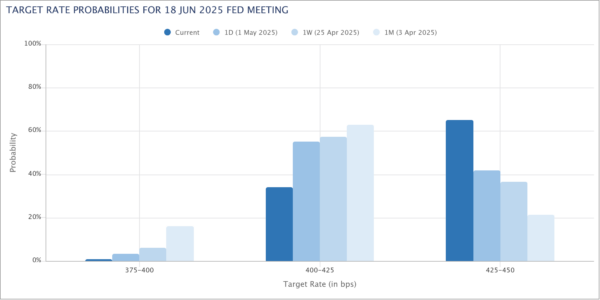

On the similar time, expectations for Fed coverage are present process a recalibration. With the labor market holding agency and inflation nonetheless persistent, the urgency for one more price lower has diminished. Fed fund futures at the moment are pricing only a 35% probability of a lower in June — down sharply from 63% every week in the past and practically 80% initially of April. Importantly, this moderation in price lower bets is being absorbed with out destructive market response, signaling that buyers are snug with Fed remaining on maintain for longer.

Technically, S&P 500’s rally from the 4835.04 low is seen because the second leg within the medium-term sample from 6147.43 document excessive. Additional upside is favored within the close to time period so long as 5433.24 help holds. However vital resistance round 6147.43 to deliver the third leg of the sample.

Within the larger image, the long run up development stays intact. S&P 500 is properly supported by long run rising channel, and managed to defend 4818.62 resistance turned help (2022 excessive).

An upside breakout is feasible through the second half of the 12 months. However that may depend upon two key parts: the decision of commerce uncertainty and continued financial resilience.

If July’s truce deadline passes with out escalation — or higher but, with concrete de-escalation — and financial knowledge stays agency, then a brand new document could be on the horizon.

Yields Rise on Threat-On Move, However Greenback Fails to Trip the Wave

US 10-year Treasury yield staged a rally rebound on Friday, in tandem with equities. Not like earlier yield spikes pushed by capital flight, this surge seems rooted in a rotation out of safe-haven belongings and into equities, as threat urge for food returned.

Technically, 10-year yield’s pull again from 4.592 has possible accomplished with three waves all the way down to 4.124. Break of 4.407 resistance will solidify this bullish case. Rise from 3.886 may then be resuming via 4.592 resistance to 100% projection of three.886 to 4.592 from 4.124 at 4.830.

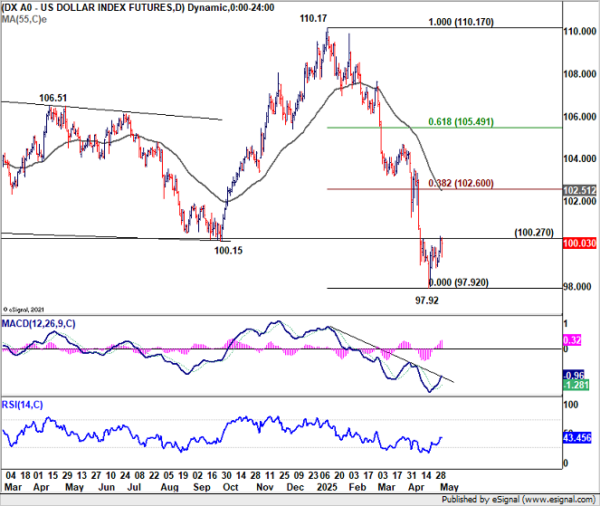

In distinction, Greenback has did not capitalize on both yield energy or decreased recession nervousness. Expectations for Fed to maintain rates of interest elevated longer could present some underlying help. But when threat sentiment continues to enhance, demand for USD as a defensive play could proceed to weaken, at the same time as yield help holds.

Technically, agency break of 100.27 resistance in Greenback Index will deliver stronger rebound again to 55 D EMA (now at 102.51). However sturdy resistance needs to be seen from 38.2% retracement of 110.17 to 97.92 at 102.60 to restrict upside.

Bullish Case Proceed to Construct for AUD/JPY, with 94.94 Fibonacci Goal in Perception

AUD/JPY ended final week as the highest winner and gained 1.56%, on a potent mixture of risk-on sentiment and modifications in financial coverage outlooks.

Aussie’s energy was bolstered by Q1 inflation knowledge from Australia. On the one hand, the trimmed imply CPI returned to RBA’s 2–3% goal vary for the primary time since 2021, cementing expectations of a Might price lower. Nonetheless, stronger than anticipated headline CPI studying, and renewed items inflation pressures factors to a cautious and gradual easing path, relatively than an aggressive cycle.

In distinction, Yen suffered after BoJ left charges unchanged and sharply downgraded its development forecast for fiscal 2025, slashing it by greater than half. Moreover, core inflation projections have been revised decrease, elevating the chance of falling in need of the two% goal once more. The downgrade has pushed again expectations of any near-term price hikes. A June transfer now appears off the desk.

Technically, the developments proceed to affirm the case that corrective fall from 109.36 (2024 excessive) has accomplished with three waves all the way down to 86.03.

Additional rally needs to be seen within the close to time period so long as 90.57 help holds, to 38.2% retracement of 109.36 to 86.03 at 94.94. Sustained break there’ll pave the best way to 61.8% retracement at 100.44.

Nonetheless, rejection by 94.94 fibonacci resistance, adopted by break of 90.57 help, will dampen this bullish view and produce retest of 86.03.

EUR/USD Weekly Outlook

EUR/USD gyrated decrease final week however recovered after hitting 1.1265. Preliminary bias stays impartial this week first. On the draw back, under 1.1265 will resume the corrective fall from 1.1572 brief time period high. However draw back needs to be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will recommend that the correction has accomplished and produce retest of 1.1572 excessive.

Within the larger image, rise from 0.9534 long run backside might be correcting the multi-decade downtrend or the beginning of a long run up development. In both case, additional rise needs to be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This may now stay the favored case so long as 55 W EMA (now at 1.0776) holds.

In the long run image, the case of long run bullish reversal is increase. Sustained break of falling channel resistance (now at round 1.1300) will argue that the down development from 1.6039 (2008 excessive) has accomplished at 0.9534. A medium time period up development ought to then comply with at the same time as a corrective transfer. Subsequent goal is 38.2% retracement of 1.6039 to 0.9534 at 1.2019.