Strong Franc Sparks Bets on SNB Negative Rates

- Franc the principle FX winner since “Liberation Day”.

- Might hit Swiss exports, lead the nation into deflation.

- How will the SNB reply: Unfavourable charges or intervention?

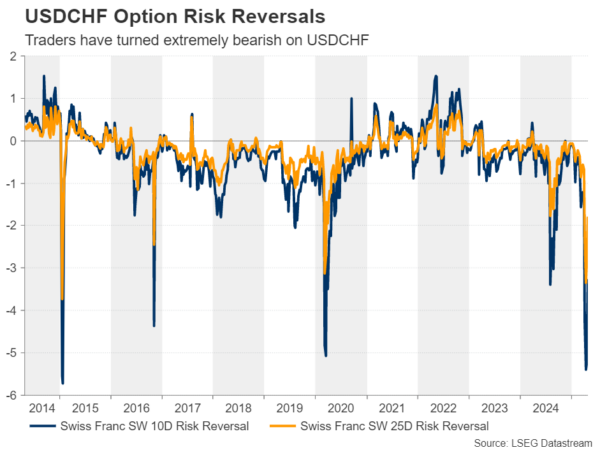

- Threat reversals level to sturdy setback ought to urge for food enhance additional.

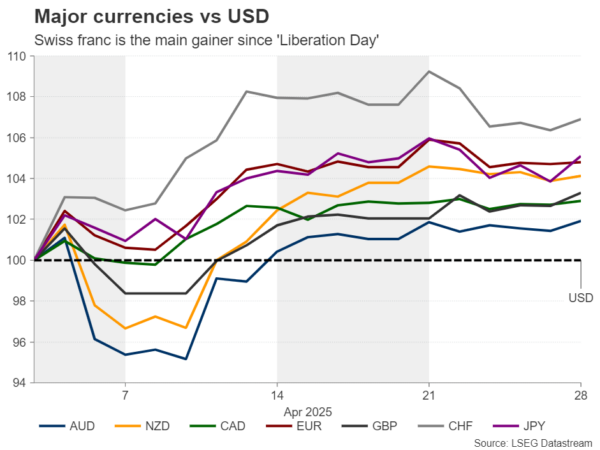

Swiss franc the final word FX haven

The Swiss franc appears to be the final word protected haven within the FX enviornment amidst the market turbulence brought on by US President Trump’s commerce coverage and the rhetoric surrounding it. Because the so-called “Liberation Day,” when Trump introduced tariffs on all of the US’s important buying and selling companion, the franc has been the very best performing main foreign money, with the opposite protected haven, the Japanese yen, taking second place. In third place, very near the yen, stands the euro, which benefited from the promoting of US belongings amid recession fears by the current fiscal shift in Germany.

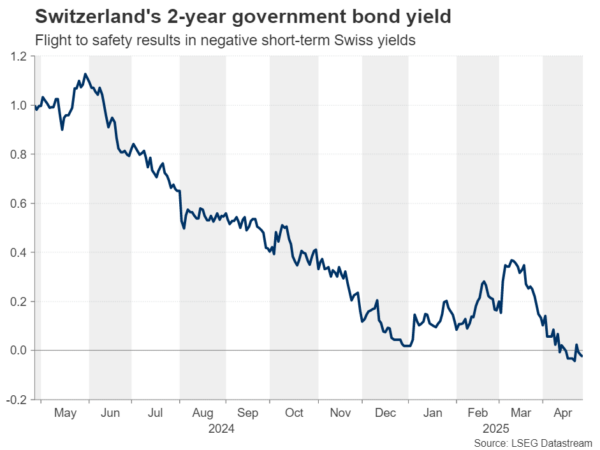

However why did the franc acquire probably the most? Why didn’t the yen observe swimsuit? Switzerland is taken into account a safe-haven vacation spot for buyers attributable to its sturdy banking and monetary system, its political stability and neutrality, its commerce surplus, its beneficial tax legal guidelines and its sturdy authorized system. Buyers have been so prepared to divert their flows there that they allowed the Swiss 2-year authorities bond yield to drop into detrimental territory. Which means buyers are prepared to lose some cash in nominal phrases in alternate for the protection of their capital. The yen didn’t carry out in an analogous method, maybe as merchants scaled again their BoJ fee hike bets amid the commerce uncertainty.

Surge threatens exporters, will increase deflation danger

Having mentioned all that, the appreciation of the franc is a serious risk to Swiss exporters because it raises the worth of what Switzerland’s buying and selling companions are paying for Swiss items. Switzerland is a internet exporting nation, and the most important importer of its merchandise is the European Union. Though the euro additionally appreciated, it didn’t shine because the franc, resulting in a drop in euro/franc and a rise within the value of Swiss merchandise in the remainder of Europe.

And the timing couldn’t be worse as US tariffs are additionally threatening Swiss exporters. On April 2, the US imposed a 31% tariff fee on Swiss items, earlier than the broader 90-day delay was introduced.

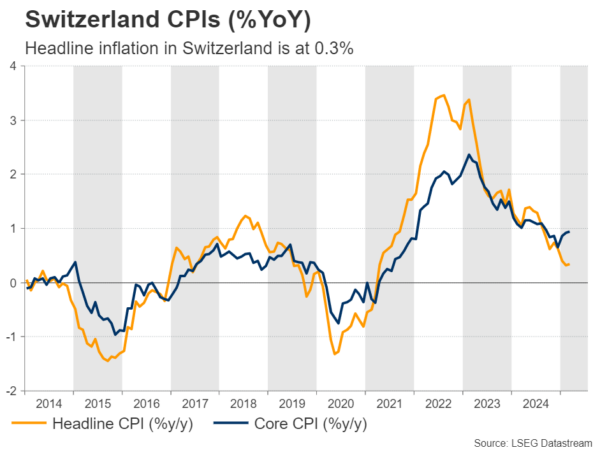

All this might weigh on Swiss inflation and it is rather more likely to lead to deflation. In any case, the year-over-year CPI fee in Switzerland is already very low, at 0.3%. And the large query on many market members’ minds these days could also be: How will the Swiss Nationwide Financial institution (SNB) reply to that?

Unfavourable rates of interest or Intervention

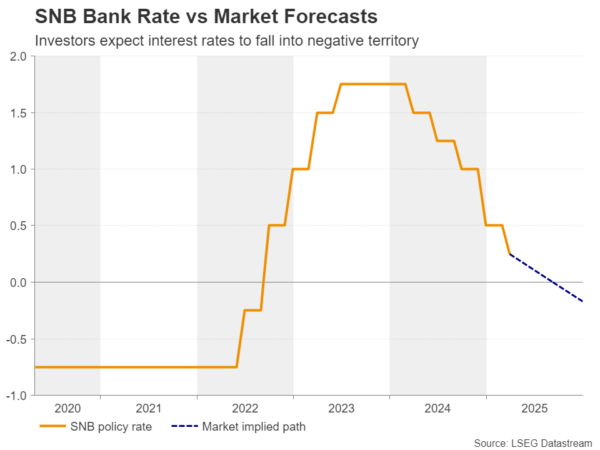

There are two channels by which the SNB had battled the appreciation of the franc. One is thru chopping rates of interest as most central banks across the globe are doing, and the opposite is thru intervention, by shopping for its personal foreign money and promoting overseas reserves.

Getting the ball rolling with rates of interest, the SNB has the bottom benchmark fee amongst main central banks, presently at 0.25%, and the franc’s appreciation might have raised hypothesis that policymakers may push rates of interest into detrimental territory once more. Certainly, in response to Switzerland’s In a single day Index Swaps (OIS) market, there’s an round 80% probability for a quarter-point lower to zero on the Financial institution’s subsequent determination on June 19, with one other 10bps price of cuts anticipated by September.

SNB Chairman Martin Sclegel has not dominated out the chance of rates of interest diving into detrimental territory however famous a number of occasions up to now that such a step wouldn’t be taken flippantly.

This makes the choice of intervention because the extra probably one. Or not? In response to a Bloomberg analyst-based survey, most members predict that the Financial institution will keep away from chopping rates of interest under zero, with solely Goldman Sachs holding such a forecast.

Nonetheless, intervention won’t come with out penalties. Such a coverage dangers stirring the US hornets’ nest, with Trump probably branding once more Switzerland as foreign money manipulator as he did again in 2020. Though this might weaken Switzerland’s negotiating hand in potential commerce talks, the President of the Swiss Confederation Karin Keller-Sutter mentioned not too long ago that she isn’t frightened about that, which retains intervention as a extra probably possibility than detrimental rates of interest.

The painless means

The painless means is for the Swiss franc to additional weaken by itself. The SNB may nonetheless lower rates of interest to zero, however officers may chorus from taking them into detrimental zone and in addition abstain from intervening. Nonetheless, for that to occur, danger aversion might have to enhance additional, pushed by new headlines about easing tariff tensions and the potential of commerce negotiations.

The Swiss franc may fall notably, resulting in spectacular rebounds in franc pairs. What helps this notion is the truth that, on April 11, the 10-day and 25-day danger reversals of greenback/franc choices hit their lowest since January 2015, when the SNB deserted the 1.20 flooring in euro/franc. This factors to extraordinarily bearish circumstances, which means that there could also be little or no room for the franc to understand additional and quite a lot of draw back potential in case the broader market setting brightens additional.

Source link